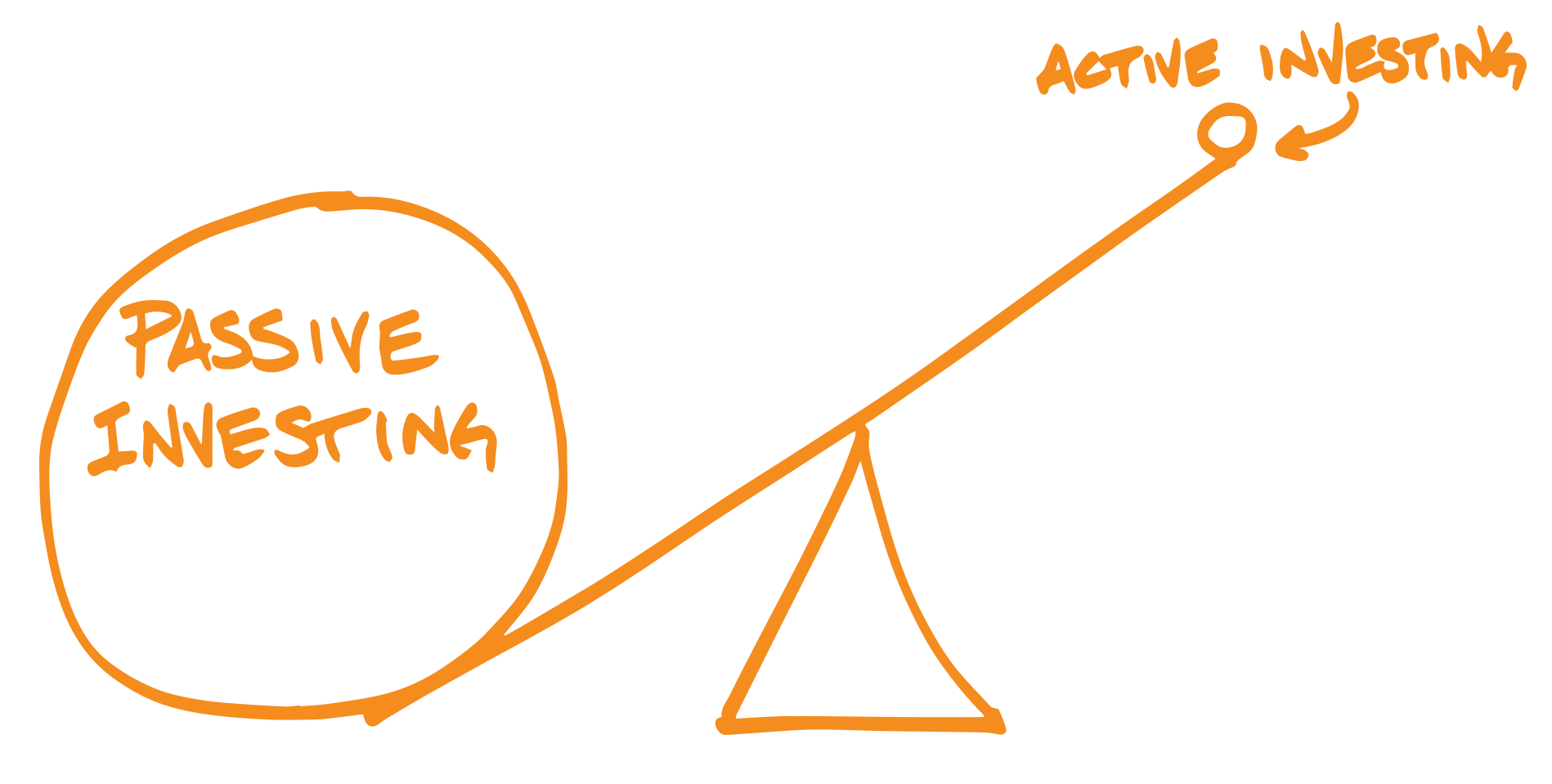

The Weight of Evidence

A SMALL SAMPLE OF ACADEMIC PAPERS THAT SUPPORT PASSIVE INVESTING

MARKOWITZ, HARRY | Portfolio selection | Journal of Finance, 1952 • FAMA, E. | Efficient capital markets: a review of theory and empirical work | Journal of Finance, 1970 • SHARPE, WILLIAM | Capital asset prices: a theory of market equilibrium under conditions of risk | Journal of Finance, 1964 • CARHART, MARK | On persistence in mutual fund performance | Journal of Finance, 1997 - FAMA, E.; FRENCH, K. | Multifactor explanations of asset pricing anomalies | Journal of Finance, 1997 • LO, ANDREW | Reconciling efficient markets with behavioral finance: the adaptive markets hypothesis | Journal of Investment Consulting, 2005 • MALKIEL, BURTON | Returns from investing in equity mutual funds 1971-1991 | Journal of Finance, 1995 • MERTON, ROBERT | Theory of rational option pricing | Bell Journal of Economics and Management Science, 1973 • SAMUELSON, PAUL | Proof that properly anticipated prices fluctuate randomly | Industrial Management Review, 1965 • BLACK, F.; SCHOLES, MYRON | The pricing of options and corporate liabilities | Journal of Political Economy, 1973 • CAMPBELL, JOHN; VUOLTEENAHO, TUOMO | Bad beta, good beta | Working Paper, 2002 • FAMA, E.; FISHER, L.; JENSEN, M.; ROLL, R. | The adjustment of stock prices to new information | International Economic Review, 1969 • MERTON, ROBERT | An intertemporal capital asset pricing model | Econometrica, 1973 • SHARPE, WILLIAM | The arithmetic of active management | The Financial Analysts’ Journal, 1991 • FAMA, E.; FRENCH, K. | The cross-section of expected stock returns | Journal of Finance, 1992 • FAMA, EUGENE; BLISS, ROBERT | The information in long-maturity forward rates | The American Economic Review, 1987 • ANAND, VINEETA | Exxon Mobil goes passive in a big way | Pensions & Investments, 2002 • ARNOTT, ROBERT; BERKIN, ANDREW; YE, JIA | How well have taxable investors been served in the 1980s and 1990s? | Journal of Portfolio Management, 2000 • ARRINGTON, GEORGE | Chasing performance through style drift | Journal of Investing, 2000 • ARSHANAPALLI, BALA; COGGIN, DANIEL; DOUKAS, JOHN | Multifactor asset pricing analysis of international value investment strategies | Journal of Portfolio Management, 1998 • BARBER, BRAD; ODEAN, TERRANCE | Trading is hazardous to your wealth: the common stock investment performance of individual investors | Journal of Finance, 2000 • BARR, PAUL | Washington system goes to indexing | Pensions & Investments, 1997 • BAUMAN, SCOTT; CONOVER, MITCHELL; Cox, Don | Are the best small companies the best investments? | Journal of Financial Research, 2002 • BAXI, NEERAJ | Paying up: the hidden cost of portfolio management, commission recapture | Journal of Investing, 2003 • BAXTER, MARIANNE; JERMANN, URBAN | The international diversification puzzle is worse than you think | The American Economic Review, 1997 • BLAKE, CHRISTOPHER; ELTON, EDWIN; GRUBER, MARTIN | The performance of bond mutual funds | Journal of Business, 1993 • BLAKE, CHRISTOPHER; MOREY, MATTHEW | Morningstar ratings and mutual fund performance | Journal of Financial & Quantitative Analysis, 2000 • BUSSE, JEFFREY; GREEN, T. CLIFTON | Market efficiency in real time | Journal of Financial Economics, 2002 - CARHART, MARK | On persistence in mutual fund performance | Journal of Finance, 1997 • CARTY, MICHAEL; NOVAK, EDWARD | Doing it with style | Financial Planning, 1997 • CHEN, NAI-FU; ZHANG, FENG | Risk and return of value stocks | Journal of Business, 1998 • COCHRANE, JOHN | Portfolio advice for a multifactor world | Fed Reserve Bank of Chicago, 1999 - COGHRANE, JOHN | New facts in finance | Fed Reserve Bank of Chicago, 1999 • COCHRANE, JOHN | The risk and return of venture capital | Journal of Financial Economics, 2005 • CONSTANTINIDES, GEORGE | Rational asset prices | Journal of Finance, 2002 • COSTA, BRUCE; PORTER, GARY | Mutual fund managers: does longevity imply expertise? | Journal of Economics and Finance, 2003 • DAVIS, JAMES; FAMA, EUGENE; FRENCH, KEN | Characteristics, covariances, and average returns 1929-1997 | Journal of Finance, 2000 • DEL GUERICO, DIANE; TKAC, PAULA | Star power: the effect of Morningstar ratings on mutual fund flows | Fed Reserve Bank of Atlanta, 2001 • DIETHER, KARL; MALLOY, CHRISTOPHER; SCHERBINA, ANNA | Differences of opinion and the cross section of stock returns | Journal of Finance, 2002 • D1MSON, ELROY; NAGEL, STEFAN; QUIGLEY, GARRETT | Capturing the value premium in the United Kingdom | Financial Analysts Journal, 2003 • DROBETZ, WOLFGANG; KOHLER, FRIEDERIKE | The contribution of asset allocation policy to portfolio performance | Financial Markets and Portfolio Management, 2002 • ELTON, EDWIN; GRUBER, MARTIN; BLAKE, CHRISTOPHER | The persistence of risk-adjusted mutual fund performance | Journal of Business, 1996 • ELTON, EDWIN; GRUBER, MARTIN; MANN, CHRISTOPHER; AGRAWAL, DEEPAK | Explaining the rate spread on corporate bonds | Journal of Finance, 2001 • EVANS, JOHN; ARCHER, STEPHEN | Diversification and the reduction of dispersion: an empirical analysis | Journal of Finance, 1968 • FORTIN, RICH; MICHELSON, STUART; JORDAN-WAGNER, JAMES | Does mutual fund manager tenure matter? | Journal of Financial Planning, 1999 • GREER, ROBERT | The nature of commodity index returns | Journal of Alt Investments, 2000 • HARRIS, RIGHARD | The accuracy, bias and efficiency of analysts’ long run earnings growth forecasts | Journal of Business Finance and Accounting, 1999 • IBBOTSON, ROGER; KAPLAN, PAUL | Does asset allocation policy explain 40%, 90%, or 100% of performance? | Working Paper, 1999 • KEIM, DONALD B. | An analysis of mutual fund design: the case of investing in small-cap stocks | Journal of Financial Economics, 1997 • KORN, DONALD JAY | Make indexing less taxing | Financial Planning, 2000 • KOZLOWSKI, ROS | Indexed assets pass $3 trillion mark for first time | Pensions & Investments, 2004 - MCGUIGAN, THOMAS | The difficulty of selecting superior mutual fund performance | FPA Journal, 2006

© 2011 Behavior Gap